Retirement and savings account contribution limits are rising for 2026, alongside a new rule affecting how higher-earning workers make catch-up contributions.

The chart below summarizes the 2025-2026 contribution limits for retirement accounts. Note the following new rule effective for 2026: if a participant had over $150,000 of FICA wages from the plan sponsor in 2025, then any catch-up contributions to that employer’s plan in 2026 must be made on a Roth/after-tax basis. Catch-up contributions are tested per employer.

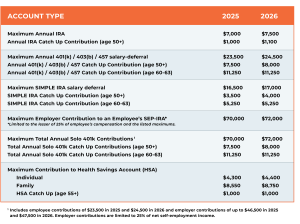

Individual Retirement Accounts (Traditional and Roth IRAs):

The annual contribution limit for under‑age‑50 participants increases to $7,500 in 2026 (from $7,000 in 2025). The catch‑up limit for those age 50 or older is $1,100 for 2026 (up from $1,000), totaling $8,600 for the year.

401(k), 403(b), 457 Plans, and Thrift Savings Plans:

For 2026, workers may elect up to $24,500 in salary deferrals, up from $23,500 in 2025. For those age 50 or above, the catch‑up contribution rises to $8,000, up from $7,500. For workers aged 60‑63 eligible for the “super” catch‑up, the limit remains $11,250 unless otherwise changed.

SIMPLE IRAs:

For 2026, the contribution limit will increase to $17,000, up from $16,500 for 2025. If you are 50 or above, you can make an additional $4,000 in catch-up contributions, totaling $21,000. For workers aged 60‑63 eligible for the “super” catch‑up, the limit remains $5,250, totaling $22,250 for the year.

SEP IRAs:

Employers contributing to an employee’s SEP-IRA can contribute the lesser of 25% of the employee’s compensation or $72,000 annually. This is a $2,000 increase from the 2025 limit, $70,000.

Solo/Individual 401(k) Plans:

The employer contribution limit will increase to the lesser of 25% of self-employment compensation or $47,500. The maximum contribution (employer plus employee) for a solo 401(k) participant will be $72,000 for those under 50, $80,000 for those age 50 or older, and $83,500 for those age 60-63 as part of the “super” catch-up.

Health Savings Accounts (HSAs):

Annual contribution limits for HSAs have increased for 2026. Individual enrolled in a qualified health plan can contribute $4,400, while families can contribute up to $8,750, with an additional $1,000 catch-up contribution for those age 55 and older.