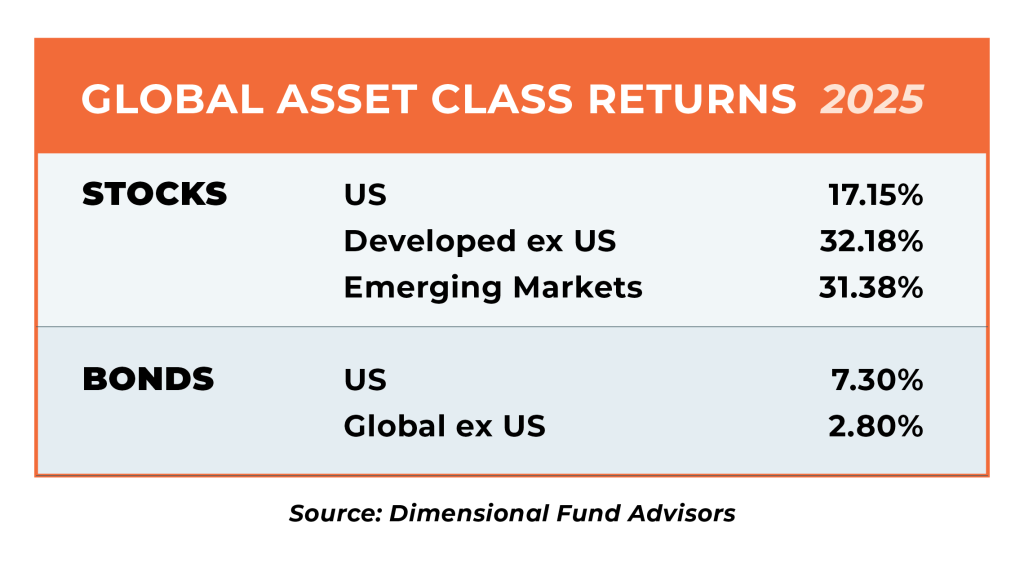

U.S. stocks rose 17.15% in 2025, marking another solid year—but this time, it was international and emerging markets that led the way. Developed markets returned 31.85%, and emerging markets surged 33.57%, significantly outpacing the U.S. for the first time in years. Meanwhile, after a challenging stretch, falling interest rates across much of the yield curve finally rewarded bond investors, as the U.S. aggregate bond index delivered a return of 7.3%—a result that went largely unnoticed.

An Extraordinary Three-Year Run

Before turning to what changed in 2025, it’s worth pausing to acknowledge just how strong the last three years have been for U.S. stocks. From the market’s rebound in 2023 through 2025, U.S. equities delivered a remarkable stretch of gains, fueled by innovation, easing inflation, and investor optimism. The Russell 3000 Index—representing the total U.S. stock market—posted a cumulative three-year return of more than 82%. Large growth companies in particular drove much of the performance, continuing a trend that had already defined much of the 2010s and early 2020s.

Global Markets Outperform…Finally!

Heading into 2025, international stocks had just come through a tough stretch. Over the prior three years, they had significantly underperformed U.S. stocks, leading many investors to question why they even owned them. In last year’s market review, we made two points: first, that staying patient with a well-balanced, globally diversified portfolio is essential. And second, that non-U.S. stocks were much cheaper than their U.S. counterparts on several valuation measures. That valuation gap, we suggested, might favor non-US stocks going forward.

What actually happened in 2025? Developed international stocks rose over 31%, and emerging markets surged even higher. Investors who stayed the course and did not abandon global diversification were handsomely rewarded.

Are Small Company Stocks Next?

Over the last few years, much of the U.S. market’s performance has come from just a small group of companies—often referred to as the “Magnificent Seven.” Meanwhile, small company stocks have lagged behind for several years now. Since the start of 2023, U.S. large-cap stocks (Russell 1000) returned approximately 84% cumulatively, while small-cap stocks (Russell 2000) delivered a return of 47%.

That lag in performance is striking, and it’s reminiscent of the gap we saw with international stocks heading into 2025. And much like we said then, small-cap stocks now look much less expensive than their large company counterparts. On basic measures like price-to-earnings and price-to-book ratios, small cap stocks are trading at some of the largest discounts to large caps we’ve seen in years.

Just like 2025 turned out to be the year international stocks made a comeback, perhaps 2026 will be the year that small company stocks shine. No one knows for sure. Either way, the diversification benefit that comes from owning small company stocks is the most important reason to own them—and that will hold true regardless of short-term performance.

Final Thoughts: Staying Grounded

The past three years have been an extraordinary run for markets, particularly in U.S. equities. Periods like this can cause us to believe that runs like this are normal and that risks of owning stocks have been mitigated or even eliminated. But we know from history, theory, and common sense that this is not true.

As a result, now may be a good time to moderate expectations, remember that bear markets are a normal part of investing, and remain steadfast in your commitment to the basics—diversification, regular rebalancing, and a sound financial plan that accounts for both good and difficult market periods.